Note: this article has been read over 100,000 times and also liked or shared hundreds of times across social media.

The Wall Street Journal (WSJ) showcased a widely-shared article [link] earlier this month exposing the fact that we have lacked 5% corrections, jointly among three main indices around the globe. This is a provocative statistical indicator, as many investors consider for their portfolio generally one market index that is heavily weighted towards their home country. The fact that other indices in foreign regions are mirroring these similar streaks could perhaps be compelling. Let’s take the U.S. for example, we've gone over a year without a 5% correction. This exact lengthy time without such a pullback has only occurred a handful of times since the mid-20th century. And while that would therefore seem extraordinarily rare, given exclusive time stages it works to about an 8% annual probability (so not that rare.) [link] What we have in Russolillo's WSJ article is a look beyond this one location, but in Europe and in Asia as well. These investors need be mindful to global economic conditions and financial markets as well. Yet the statistic in the WSJ article focuses on the 5% correction dearth not being just over a year -as it is in the U.S.- but rather the three indices going dropless for the first half of 2017. This article resolves how one should think about these two different probabilities.

* How do we consider seasonality in the markets?

* How correlated are these markets, and what is the import of selecting just this year-to-date as the time horizon?

* What should an investor or risk executive do in consideration of this insight?

The Wall Street Journal (WSJ) showcased a widely-shared article [link] earlier this month exposing the fact that we have lacked 5% corrections, jointly among three main indices around the globe. This is a provocative statistical indicator, as many investors consider for their portfolio generally one market index that is heavily weighted towards their home country. The fact that other indices in foreign regions are mirroring these similar streaks could perhaps be compelling. Let’s take the U.S. for example, we've gone over a year without a 5% correction. This exact lengthy time without such a pullback has only occurred a handful of times since the mid-20th century. And while that would therefore seem extraordinarily rare, given exclusive time stages it works to about an 8% annual probability (so not that rare.) [link] What we have in Russolillo's WSJ article is a look beyond this one location, but in Europe and in Asia as well. These investors need be mindful to global economic conditions and financial markets as well. Yet the statistic in the WSJ article focuses on the 5% correction dearth not being just over a year -as it is in the U.S.- but rather the three indices going dropless for the first half of 2017. This article resolves how one should think about these two different probabilities.

In other words, their article gives birth to various attractive

mathematical and finance, contexts and impacts.

For example, here are some questions one might ponder from such a

finding:

* What

is the mathematical probability of seeing such a result?* How do we consider seasonality in the markets?

* How correlated are these markets, and what is the import of selecting just this year-to-date as the time horizon?

* What should an investor or risk executive do in consideration of this insight?

And in the examination below, we focus equal time on all

four of these questions. Starting with

the first three bullets above taken as one section.

Probability,

seasonality, modeling parameters:

There are multiple theoretical ways to determine the rarity

of this three indices event. This is

complicated by the length of historical data accompanying with the markets, in

addition to the internal composition of the index (e.g., the U.S. markets are

currently more weighted to technology, while in the previous crisis it was

weighted more towards financials.)

Because we are looking at frequency of occurrences, the

Poisson distribution work better than a Gaussian distribution. Even still, we are looking to fit a threshold

level of an extreme tail event (a near-record streak without a 5%

correction.) After this we have the

challenge of fitting three partially-correlated indices that are concurrently

all at this same rare streak (we don't seek the convolution probability of not

seeing one (out of the three) index with this rare streak, but rather all three

jointly showing this dripless streak.)

Note that this is not the same thing at all to asking the question of

whether the three indices are correlated in terms of their amount of daily

change (e.g., two indices can trend up but have no correlation, and vice-versa). There are clearly covariance (e.g., financial

Beta measures), and tail concordance [link],

and other differences to contend with as this is not a matter of the main of

these distributions.

A standard trivariate normal distribution could be used for

the theoretical model, and then mapped to the non-parametric results we are bearing

in mind. And we do this even though

there tends to be seasonality in risk, there is also wide dispersion in the

same (the 2015 summer and winter flanking that year’s autumn had the most

petrifying crashes in recent years). Leveraging

the understanding of an individual market index is key, and strengthens the probability

support of the (obviously scarcer) probability model we seek, for all three

indices jointly.

This could be a challenge (though obviously doable) in

closed form for just any two indices, and it becomes even thornier if we hope

to expand the correlated probability framework to multiple indices. This is the charm in what the WSJ article

exposes by looking at major financial hubs around the world. There is no need to elucidate all of the

mathematical proof here in this article, since it has already been solved for [link]

and works well for any level of multi-colinearity except for perfect negative

linear-correlation (which we obviously don't have in financial markets).

Transferring an approximation of the covariances and

underlying correlations, it seems appropriate to calibrate the question to

something along the lines of this: if three markets each have a 15% chance of

NOT seeing a 5% correction over the first half of the year, and these

underlying streaks are 2/3 correlated with one another (correlation in this

observed rare streak, obviously not general correlation in market

trends/changes themselves), then what's how rare would it be the see all three

indices to jointly lack this 5% correction?

[link,

link] In terms of the 2/3 correlation, realize that

once one is in a trend that is partially correlated, it is even more difficult

to see repeated daily changes on the other side of that trend. Hence, we see that the correlation in the infrequent streaks away from the trend

is more distinct than the

correlation in any price change relative

to a common trend.

And here we see the answer is roughly a 6% semi-annual probability,

or less rare and more fat-tailed than the >30 recent years noted empirically in the WSJ article, and again

working with the practical 15% single-index assumption. Except here it is solved with more underlying

data on one comparable index, and considers framing the probability problem in

a hypothesis testing format. Also, a

bonus probability question, if one has 50 years of market history starting with

a rare event (e.g., a streak) that wasn’t again seen until now, then how rare

is that event? Is it a 1:50 year event,

or perhaps something more or less? The

answer here gets into the topic of degrees of freedom and how we anchor

probabilities based on just seeing an observation and then treating it as a

normal observation as opposed to knowing your entire analysis is conditional

upon starting the clock with the forced inclusion of such special observation.

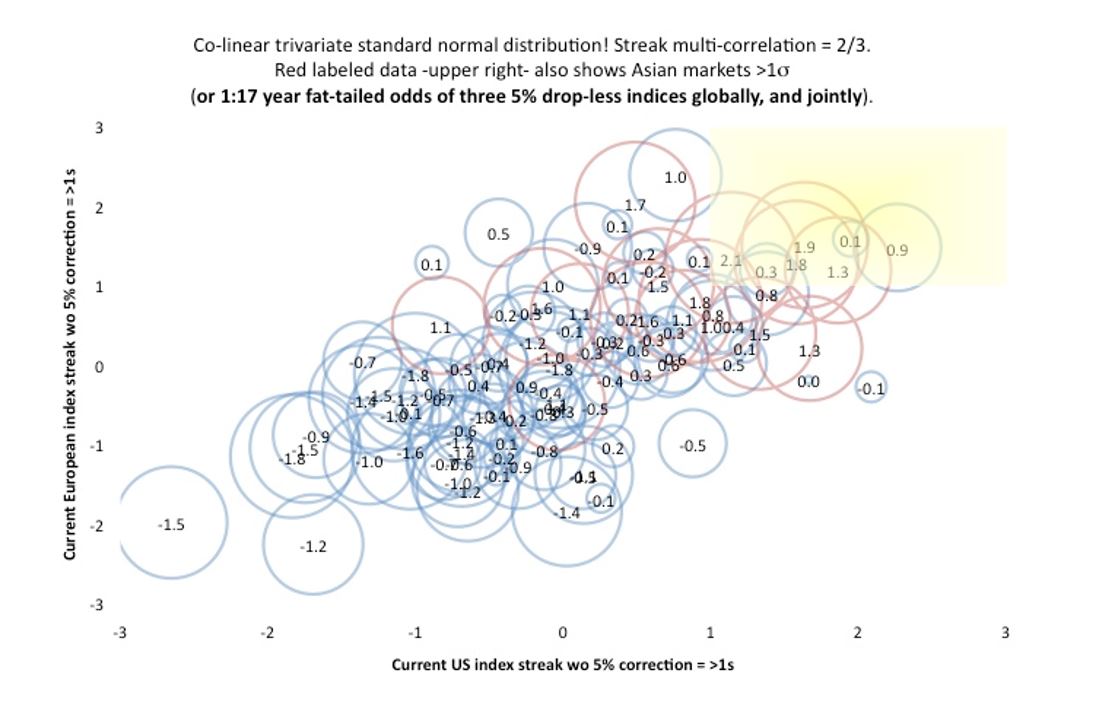

Incidentally the chart above shows a simulated visual (n=1000)

of how one might consider the problem, where the horizontal and vertical axes

represent two markets, and the third dimension (for depth, and one we

facilitate by showing it in varying size and the level marked as a label)

represent the third market. The red data

simulated shows where the third market is in the 15% rare streak without the 5%

correction, and the overall joint probability comports to the same 6% discussed

above.

Now it is worth noting that an 8% probability in the U.S.

over a given year is more likely than a 6% semi-annual probability. We can

see this as the probability of the U.S. correction-less streak on a semi-annual

basis is greater than 8% of course (we solve it above as 15%!), so therefore higher

than 6%. So, the WSJ touched upon an

exciting rare streak, though at 6% semi-annual odds, it is simply not that

rare.

Instead, as we discuss below, we should consider the other complimentary yet rarer streaks we have. For example, the

lack of a 1% down day in months, and even the lack of a 3% down-day or even a

3% correction relative to the normal historic frequency of the same.

What should an

investor do?

5% corrections (defined as an interruption of a bull market,

and not the daily oscillations we saw during the financial crisis) provide a

buying opportunity, and the rarer a streak has been without such a correction,

the more likely it is to occur sooner rather than later, as markets revert.

In this market, we are due for any range of down-turns, from

the 1% drop to the 10% corrections. However,

we have had a few tail risk events in 2015, which is more frequent than usual,

subsumes the smaller corrections we are discussing here, and also makes up for

a steady climb since. Now the newly

confident, the younger, or more risk hungry, the investor is the less likely

they may have their portfolio positioned for such an eventuality [link, link & link],

as recent experience might cause investors to falsely and optimistically

conclude that the rare streaks now without 5% corrections is "more standard".

Nonetheless, we are due for this level of sell-off, even if

it comes in the form of a slow and choppy grind lower. One where the various indices drop without as

much of a rise in implied volatility or gamma.

No one knows precisely when or at what speed various markets will sell

off a few percent, or even more than 5%.

The correction can easily defy historical frequency and severity patterns. It is fair to assume that each of these

indices will see their 5% or worse correction, but there is no evidence that they will

see it right away. Staying liquid is

important to position one’s portfolio for such an eventuality, and avoid taking

so much risk now and hoping to beat the ultimate surprise, stampede for the

doors. Also, it should be noted that if any one index drops 5%, one's individual holdings (to the degree they are different

than that one index) can drop significantly more than 5%. Diversifying globally of course is a

wonderful idea (second only to de-risking), though being mindful that market and currency fluctuations can

swerve from the 5% level of any one index drop.

No comments:

Post a Comment